Backed by structural advantages and robust fundamentals, the Middle East and Africa region is expected to record sustained GDP growth rates over the medium to longer term, Credit Suisse analysts said in July.

Addressing participants at a Credit Suisse Research Roundtable, Kamran Butt, head of Middle East Equities Research at Credit Suisse, Private Banking, said, “In our view, stable oil prices and improved business confidence will be the major catalysts for a robust rebound in GDP growth in 2010. While the region is set to witness improved economic conditions across all markets, the growth in GDP will not be evenly distributed with Qatar leading in 2010.”

Commenting on regional markets, Mohamad Hawa, head of MENA Equity Strategy and Financials Research at Credit Suisse, Investment Banking, said, “MENA markets, although flat year-todate, have managed to outperform GEM and EMEA equities, which suffered from fear of contagion effect from Greece, Hungary, and the possibility of slowdown in China.”

Explaining the region’s diverse investment terrain, Hawa said that Abu Dhabi banks looked attractive and Qatar was a preferred market due to its high economic growth. Egypt reflected strong fundamentals and an under-leveraged economy but was weighed down by slowing FDI and rich valuations. Overall, Middle-East banks had outperformed their global peers, with Saudi banks returning 9.5 per cent.

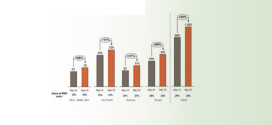

Presenting an economic overview of the region, Butt said that within the GCC, Qatar was expected to achieve the highest GDP growth rate for the second consecutive year in 2010 – estimated at 18.5 per cent. “This growth will be driven by expansion of LNG production and the non-hydrocarbon sectors of the economy. In line with our positive economic outlook for 2010, supported by stronger energy prices, we believe that fiscal and external accounts will most likely reach surpluses.” The impact of the global financial crisis has been limited in Qatar due to timely and supportive macroeconomic policies and intervention in the local banking system. The main risks to the short-term economic outlook were unexpected construction delays, a considerable negative external demand shock, lower hydrocarbon prices and a further decline in real estate prices.

Overall, the current account balances of oil exporting countries were expected to benefit from improved oil prices. Demand had started to recover in emerging markets as well as industrialised countries, which should be “supportive for prices in the long run”.

According to Butt, strong external and fiscal positions prior to the global recession allowed GCC economies to implement measures in response to the downturn. When the shadow of the financial crisis swept the region, almost all countries provided liquidity support, while a majority of them opted for monetary easing, with Saudi Arabia, UAE and Kuwait guaranteeing deposits, he added.