Caroline Maginn looks at one of the growing number of companies in the KSA that is transforming itself into an international powerhouse

The new corporate powerhouses in MENA started to announce further progress la st year and it is a very exciting time to be a progressive corporate in the KSA, pro-active in the commercial equivalent of London’s financial Big Bang of the 1980s.

st year and it is a very exciting time to be a progressive corporate in the KSA, pro-active in the commercial equivalent of London’s financial Big Bang of the 1980s.

Similarly to the way that banks stretched their boundaries then, a growing group of home-grown companies have undergone a transformation in this millennium by restructuring their production and/or sourcing, expanding their domestic market penetration and successfully tapping regional and overseas export markets on the back of strong brand and quality.

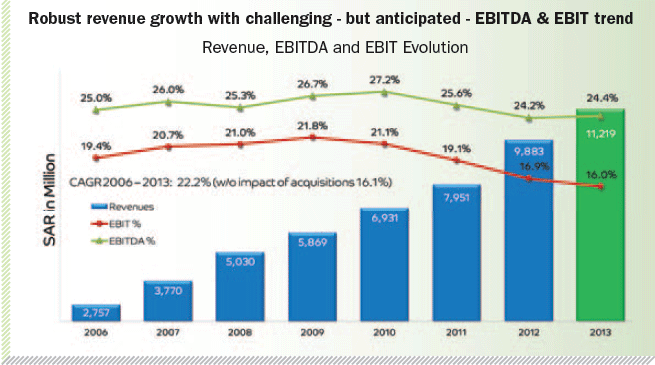

Almarai is one such company. It evolved a multi-pronged strategy to transform both the dairy farming and food production industry in the KSA to become one of the world’s largest vertically integrated dairy businesses. The company has balanced its investment by continually upgrading its traditional business lines to increase quality whilst diversifying its product base with fruit juices, bakery, poultry and, latterly, infant products; thus generating a healthy earnings growth to its broadening investor base of more than 70,000 shareholders. It is an example in action of the country’s shift from import substitution to export promotion in the non-oil related flows.

Its acquisition and capex spend in its strategic lines continued apace in 2013 with a tightly managed control of the EBITA challenge and an innovative approach to managing debt diversification. This was fundamental to its ability to manage the cash flow bridge. Additionally, it added to the depth and breadth of funding relationships beyond banks whilst also using its healthy revenues to fund growth.

Its financial success is the lagging indicator of its strategically planned and meticulously executed business success. Its business strategy, which has been wholesome since it first started in the 1970s as a private company to serve its customers with high quality nutritious food, has always been brave and progressive.

It has also ventured into geographical markets, such as Argentina and Egypt that others considered

too risky.

With one of its latest ventures, infant products, developed as a joint venture with Mead Johnson, it is now autonomous and independent. With poultry, which it started in 2009, one of its later ventures, it is quite honest regarding the challenges it faces but takes heart and reasoned optimism because of its stamina in other businesses in the past and its ability to add industrial scale and capacity in a largely family run sector to meet the sizeable local demand in the KSA and wider MENA for a quality product.

With one of its latest ventures, infant products, developed as a joint venture with Mead Johnson, it is now autonomous and independent. With poultry, which it started in 2009, one of its later ventures, it is quite honest regarding the challenges it faces but takes heart and reasoned optimism because of its stamina in other businesses in the past and its ability to add industrial scale and capacity in a largely family run sector to meet the sizeable local demand in the KSA and wider MENA for a quality product.

Developing an increasingly balanced business portfolio to serve its growing satisfied customer base has been the result of a layered tactical approach to strategic partners, namely:

Developing an increasingly balanced business portfolio to serve its growing satisfied customer base has been the result of a layered tactical approach to strategic partners, namely:

- developing one of the largest vertically integrated dairy food businesses in the world by rationalising and merging originally small, privately owned farms into a centrally managed manufacturing and sales operation with leading technology and human know-how

selectively partnering with best-in-class companies such as PepsiCo, in fruit juices, and Mead Johnson in its infant products has been a cornerstone of its success. In the latter, now that it has achieved production excellence according to Mead Johnson’s own quality control, it has developed and had the confidence in its internal talent to go on to assume 100 per cent management control and ownership of its operations. This was done by amicable agreement ratified by both parties in 2013

selectively partnering with best-in-class companies such as PepsiCo, in fruit juices, and Mead Johnson in its infant products has been a cornerstone of its success. In the latter, now that it has achieved production excellence according to Mead Johnson’s own quality control, it has developed and had the confidence in its internal talent to go on to assume 100 per cent management control and ownership of its operations. This was done by amicable agreement ratified by both parties in 2013- developing sophisticated highly targeted sourcing of the ingredients that go into their products – eg mangoes from India and guavas from Egypt

- long-term investments and more vertical integration to secure and control the cost of critical and sizeable supply lines of feedstock through investment in plantations in Poland, Ukraine and Argentina. This makes them both more self-sustaining and financially less vulnerable to international commodity prices. Fondomonte in Argentina is eventually expected to supply 20 per cent of the company’s feedstock need and is/was on target to deliver its first shipment in Q4 2013

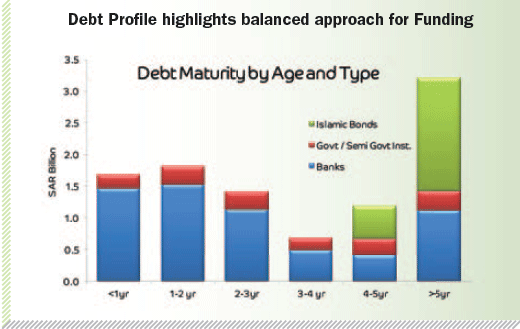

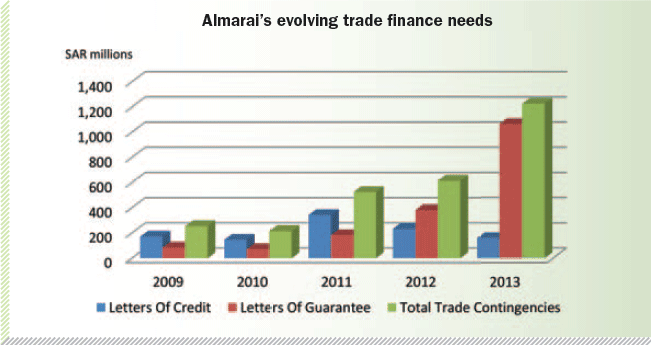

- tightly managed financing, across the company, to fund working capital requirements from the growing business itself, as far as possible, and a broad network of Islamic and Conventional Islamic Financing solutions, including trade finance and cash management. This has been with an almost text book model-like management of diversified funding and of bank lines and charges (reduced in 2013) and a cost of financing required over time – such as could only be wished for by many other companies. In effect, it is a paradigm banking shift in banking relations and financial management. In a matter of years it has switched from the loan side of a bank balance sheet to the investment side with a “perpetual” sukuk, sold very selectively to a mixed group of local and foreign banks and investors and become a listed company with robust financial indicators

- shifting away from letters of credit to guarantees and open account for its rising trade finance needs, leveraging its trusted buyer status and negotiating power to reduce its cost of goods purchased.

The evidence of Almarai’s thought-out bravery is exemplified very clearly by its diversification in Argentina and Egypt, among others.

In Argentina, for example, the company is not unduly concerned about the potentially adverse political stability negatively affecting this supply chain. It worked to make it become a reality. It is an Almarai-style case study – making long-term investments to manage forward, long-term, the cost of production and the vulnerability of supply and P&L erosion of volatile open market supply side costs. Its seasoned understanding of the markets and belief that Argentina will deliver exports, which, come rain or shine, are that country’s lender of last resort and principal cash stand-by underpinning its keenness to release exports to realise the receipts can be, in fact, a strength at times of political instability.

In Argentina, for example, the company is not unduly concerned about the potentially adverse political stability negatively affecting this supply chain. It worked to make it become a reality. It is an Almarai-style case study – making long-term investments to manage forward, long-term, the cost of production and the vulnerability of supply and P&L erosion of volatile open market supply side costs. Its seasoned understanding of the markets and belief that Argentina will deliver exports, which, come rain or shine, are that country’s lender of last resort and principal cash stand-by underpinning its keenness to release exports to realise the receipts can be, in fact, a strength at times of political instability.

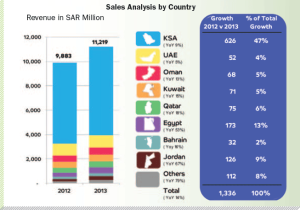

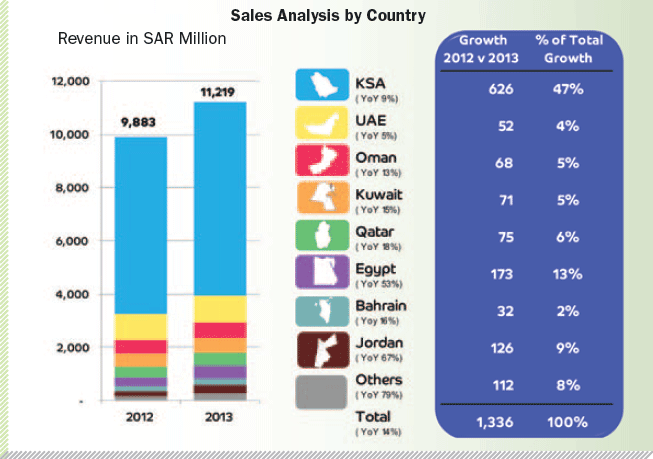

In Egypt, Almarai expanded its footprint at a time when others paled and, regrettably, sometimes failed. Despite the fact that new ventures are not without their teething problems, or for the faint-hearted, Almarai has been active in sourcing ingredients, farming production of juices and dairy products for exports. It gathered experience of the Egyptian market through its sourcing activities for fruit, selling its dairy products and, latterly, infant nutrition products. Based on market knowledge, it progressed to invest in building a farm and manufacturing capability, all supported by a state-of-the-art logistics operation at its sales depot.

In Egypt, Almarai expanded its footprint at a time when others paled and, regrettably, sometimes failed. Despite the fact that new ventures are not without their teething problems, or for the faint-hearted, Almarai has been active in sourcing ingredients, farming production of juices and dairy products for exports. It gathered experience of the Egyptian market through its sourcing activities for fruit, selling its dairy products and, latterly, infant nutrition products. Based on market knowledge, it progressed to invest in building a farm and manufacturing capability, all supported by a state-of-the-art logistics operation at its sales depot.

Whilst international analysts recently quizzed the company on its full-year results and, in particular, about mortality rates in poultry, its CFO Paul Gay spoke with depth and honesty about the firm’s challenges and with resonant enthusiasm about its very real successes in Egypt and elsewhere and the investment and know-how being applied to improve the productive life-span of the company flock, as well as tapping into sizeable demand and capitalising on growth opportunities.

Whilst international analysts recently quizzed the company on its full-year results and, in particular, about mortality rates in poultry, its CFO Paul Gay spoke with depth and honesty about the firm’s challenges and with resonant enthusiasm about its very real successes in Egypt and elsewhere and the investment and know-how being applied to improve the productive life-span of the company flock, as well as tapping into sizeable demand and capitalising on growth opportunities.

In summary, the company has succeeded with both financial and commercial integration and is one to watch as a brand for the future according to, amongst others, Credit Suisse and the Financial Times. It is a fine example of the type of new generation industrialisation that is achievable in the KSA – and other GCC countries – and it has some real spring in its step.

Unsurprisingly, Almarai will expect a lot from its trade finance and cash management providers in the management of its increasingly diverse business lines with the attendant risks and the need for transparency and efficiency on a day-to-day basis across a growing volume of everyday transactions.

Banks can expect to have to innovate to meet the company’s needs. Almarai’s growth potential and track record lends itself to innovative structures for trade finance and creative arguments for credit committee approvals, whether from bank funding or from other institutional investors.

In fact, bankers are already competing for invitations to Almarai’s increasingly rich table.