CAROLINE MAGINN wonders whether there are other relationships in the Gulf Co-operation Council states that merchant financiers should be cementing

CAROLINE MAGINN wonders whether there are other relationships in the Gulf Co-operation Council states that merchant financiers should be cementing

There is, arguably, much global debate, mind-set and misnomer centred on the premise that natural resource abundance, particularly minerals, can have adverse consequences for social well-being, political stability, the environment and sustainable economic growth and creates a parallel disadvantage between suppliers and their buyers; the so-called resource curse.

As to who benefits and who suffers, this is argued to and fro between parties at both ends of the buy and supply chain.

The arguments are detailed, lengthy and often repetitive. However, the whys and wherefores are a secondary point when it comes to turning the wheels of cars, factory belts or powering mobile phone chips and, latterly, the cloud.

Rare earth mineral resources have always been topical, controversial and commanded a premium and will likely continue in that manner. Those who direct liquidity from most recent trade surpluses are those who typically foot the goodwill bill for upcoming generations.

At present in the GCC there is a confluence of rare earth mineral reserves, liquidity and investment in industry and the built landscape. This is evident in many industry segments both glamorous and unglamorous.

Consistently since the 1980s construction and, behind that, the exploration for building materials, relevant minerals and the manufacturing plant and expertise has received strategic oversight and investment. This has been to make meaningful progress in enlightened production and includes the second generation of the region’s successful heavy engineering wave following what is known as black gold. That countries such as the KSA still have “white gold” is neither here nor there but it is overlooked.

In recent years there has been widespread due diligence and investment by KSA stakeholders to expand:

- geological surveys for raw materials

- efficiency of power supplies

- reduction in negative environmental impacts of production

- enhancement of manufacturing excellence and cost competitiveness

- production of needed cement through new, expanded and/or improved cement lines

Globally, the development of an environmentally sounder footprint, with the benefit of advances since industry partners shaped the post-World War II re-construction of infrastructure, has been a consideration for today’s cement manufacturers, including those who have been building production capacity and inventory in the GCC itself.

The cement potential being realised in the region involves domestic, intra-regional and, potentially, preferred supplier propositions. These propositions include domestic supply, regional GCC supply and wider Pan-Arab and other global market supply chains.

The government and corporate primary natural risk-takers have committed financial, intellectual and manpower capital to evolve the local supply and inventory of needed construction materials to meet strategic project needs whilst being mindful of complex environmental MENA green future issues.

banking partners on-side to make appropriate

provisions for clean liquidity going forward

The KSA joined with the World Business Council for Sustainable Development (WBCSD) survey in benchmarking more than 600 cement plants. All were visited to experience the methodology, targets were set for existing plants, a maximum energy intensity was defined for the design of new plants, and new roles and responsibilities were developed.

In addition, the Saudi Energy Efficiency Programme (SEEP) is looking at enhancing its mandate to include the collection of data, the setting of targets and their enforcement.

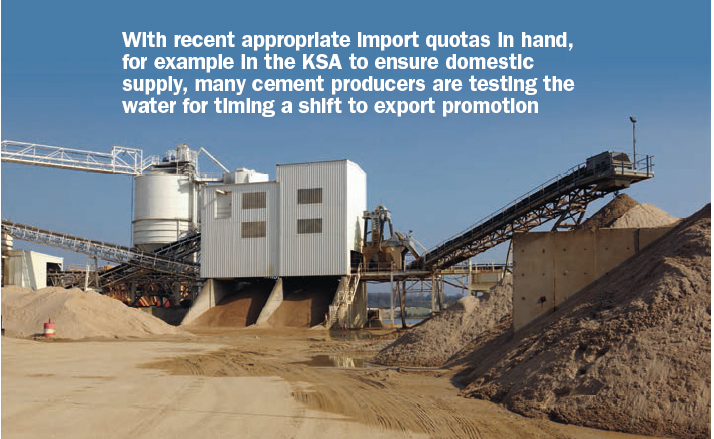

Current inventory and recent peaking, seasonal drop in sales and the rising cost of current working capital tied up in current assets is creating appetite amongst local cement producers to argue in favour of export promotion.

With recent appropriate import quotas in hand, for example in the KSA to ensure domestic supply, many cement producers are testing the water for timing a shift to export promotion and cement company equity prices are attracting increasing levels of scrutiny at present.

The region has tapped many relevant resources to mine and manufacture this inventory. It has added visible and invisible value to do so and is naturally looking to accrue some associated direct and indirect benefits at home in the form of jobs and housing for its rising population and now potentially abroad.

It will undoubtedly be doing so with caution under the framework approved by, and in consultation with, the government.

However, their would-be trade banking partners have more to do to apply due diligence screens and come up the industry learning curve as they previously did in fuel-related minerals to supply the know-how and the appropriate short- to long-term liquidity.

The cement sub-industry sector, as well as several others in building materials and construction, will most likely be featuring on Credit and ALCO committees going forward for further capex needs, M&A, prudent export finance risk mitigation and receivables and payables financings, inter-alia.

The cement manufacturers will need their banking partners on-side to make appropriate provisions for clean liquidity going forward.

Cement can be cleaner and serve a very valuable socio and economic role in the region by, quite literally, binding buildings, infrastructures and trading relationships.

The GCC cement industry, in summary, can go to proving the point that the region’s manufacturers and bankers don’t equate development of mineral resources with simply “windfalls” and “booms”.

Mineral exploration and associated production is not merely depletion of an invariable natural endowment. More to the point, the upcoming industry segments can show that so-called non-renewable resources have been, and can continue to be, progressively extended through exploration, technological progress, geological research and investments.

In the case of the GCC, this is coupled with a physical co-location with much need, transportation, geological and other rising intellectual capital, manufacturing and logistics management know-how and excellence.

Beyond the currently topical issue of clinker inventory there is much further value-added in the building materials and construction sectors pipelines.

For the construction industry in the Middle-East, especially residential, a Wood Wool Cement Board (WWCB) could provide comfortable living conditions. It could be implemented in all kinds of building concepts (new and renovation). In combination with concrete it could form well-insulated walls that could replace fired bricks.

Considering the potential for all kinds of residential housing in the Middle-East, WWCB is an attractive business proposition for cement producers and cement converters in the region, and could also provide green low-cost housing solutions. To sum up, it could be a useful tool to provide sustainable housing that may help in rejuvenating the green building industry in the Middle East.

Further alternative fuels, such as refuse-derived fuels or “RDF”, have very good energy-saving potential. The substitution of fossil fuel by alternative sources of energy is common practice in the European cement industry. The German cement industry, for example, substitutes approximately 61 per cent of its fossil fuel demand. Typical alternative fuels available in MENA countries are municipal solid wastes, agro-industrial wastes, industrial wastes and crop residues.

Solid waste disposal is a case in point not least in in the GCC. Recycling of the same will not only ease the environmental situation but also provide an attractive fuel for the regional cement industry as can agricultural waste from several MENA country partners of the GCC.

Hence the cement industry can demonstrably play a significant role in the sustainable development by the GCC and their natural trading partners. The region with its growing population can play a lead contribution to the evolution of green building materials production by leading the way in tapping alternative fuel supplies to power production.

Cement companies have done much and, of course, have many further projects in hand to contribute to sustainability by improving their own internal practices in energy efficiency and implementing recycling programs.

Businesses can show continued commitments to sustainability through voluntarily adopting the concepts of social and environmental responsibilities, implementing cleaner production practices, and accepting extended responsibilities for their products.

However, they can only do so on the basis that they find a widening pool of financial and commercial risk-sharing partners to co-sponsor them on a revolving long-term basis. Arabian Light is not the only mineral mined, manufactured and exported from the GCC to support global need and demand over the years. The world markets for white gold, frankincense, peridot, phosphates, and magnetite have shown this at different points of the past and are increasingly explored for the future.

The rapidly evolving Sukkuk market suggests new financial partners in the form of long-term bank and non-bank investors and central bank regulators investors to match the same.

Among others, The US-Saudi Arabian Business Council (USSABC) says, “The Saudi mining sector is poised for significant growth in the coming years, and the government recognises that private sector participation is required to develop a sophisticated industry with optimised output.”

The KSA is not going it alone as it has demonstrated in many financial and other arenas (the Basel Committee, the Islamic Development Bank, and Sharia Compliant Consumer and Corporate Banking), geological surveys and relevant field studies – even those to support space exploration efforts – among others.

For example, the KSA government and Ma’aden have implemented measures that make it easier for international businesses to take advantage of the Kingdom’s rich mineral resources and concurrent business opportunities related to exploration, extraction, transportation, engineering, and construction.

Cement is not a new story in the KSA; it is an unfolding one of many emerging industries in the GCC. It has many faces. n

BOX FOR TAJARA

Positive signals on exports

Saudi cement manufacturers currently talking to the government to resume exports after lower demand in the second half of 2014 created a surplus of nearly 22 million tonnes, a newspaper in the Gulf Kingdom reported recently.

“We will again meet with ministry of trade and industry officials to discuss the resumption of cement exports,” chairman of the national committee of Saudi cement companies Jihad Al Rasheed told the Arabic language daily Al Eqtisadiah.

He said previous talks have made progress and that the committee received “positive signals” from the government to allow cement producers to export their surplus.

He added that he expected consumption to recover to about 35 million tonnes in the first half of this year, pointing out that this would allow cement factories to boost sales. He told the paper that markets to be targeted by cement exporters include Egypt, Yemen, Iraq, Sudan, Ethiopia and Eritrea.