Monday 30th September 2013

- Invesco launches Global Sovereign Investor Model – a framework for understanding sovereign investor investment objectives and preferences

- Perceived quality of shareholder protection is a key driver of sovereign home market asset allocations in the West

- Latin American governments fear of ‘Dutch disease’ and have a preference for international investing

- Economies of UK and Continental Europe are losing out on new global sovereign flows, while emerging markets are the winners

Invesco today released its first Invesco Global Sovereign Asset Management Study1, an in-depth report which offers insight into the complex investment behaviour of sovereign investors across the globe.

Invesco today released its first Invesco Global Sovereign Asset Management Study1, an in-depth report which offers insight into the complex investment behaviour of sovereign investors across the globe.

The study, which provides a framework to help understand the investment preferences of these funds, finds that while sovereign portfolios are currently concentrated towards North America and other developed markets in Asia Pacific, the winners of new global sovereign flow are Emerging Markets.

Economies such as the UK and Continental Europe are currently the net losers in terms of new global sovereign flow; with both feeling the effects of significant home market investment bias across a huge swathe of sovereigns. In addition, some European sovereigns, notably pensions funds, are avoiding other international stock markets, citing major concerns over shareholder rights as a reason to invest in their local market.

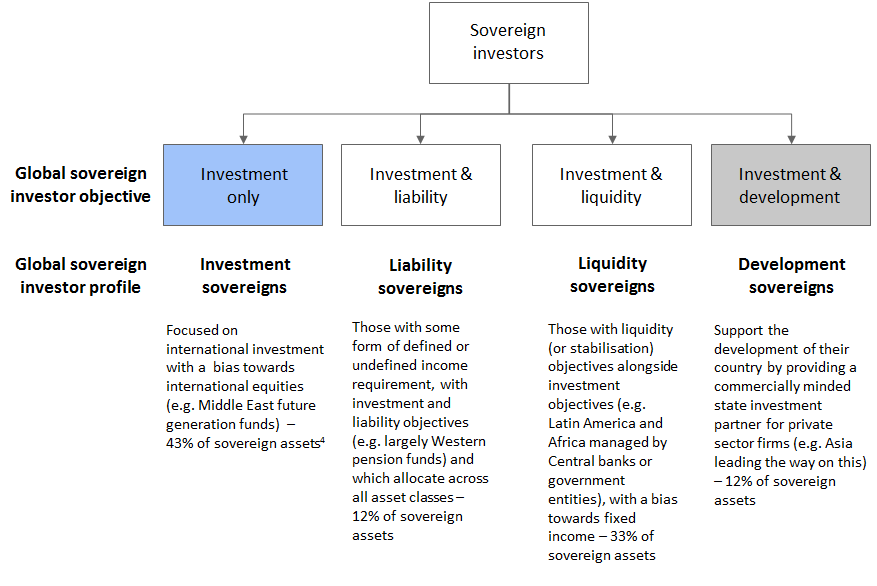

The ‘Invesco Global Sovereign Investor Model’ is an evolution from the framework developed in Invesco’s Middle East Asset Management Study2, which is now in its fourth year. It acknowledges the diversity among sovereign investors, and that each has many aspects influencing investment strategy such as region, size, environment and most importantly, investment objective.

Currently global sovereign flows represent just over US$6 trillion3, a vast market which major global economies rely on for investment. Understanding how and why these assets are being invested is therefore vital for global economies courting these sovereigns.

The Invesco Global Sovereign Investor Model bases its segmentation on investment objectives and outlines four key profiles:

Source: Invesco Global Sovereign Asset Management Study 2013

4 Based on the sample of 37 global sovereign investors

At a broad portfolio level, looking across all global sovereigns, the study found they are strongly oriented towards developed markets5 and the US in particular (33% of all asset allocations) and other developed markets, due to their relatively conservative risk appetite, a lack of capacity in emerging markets and an ability to achieve some emerging market equity exposure via developed market stocks. While sovereigns seeking to improve diversification, re-balance portfolios towards GDP and benefit from future drivers of growth, are increasingly allocating new assets to emerging markets, with Africa (33%) and China (30%) the biggest beneficiaries (based on net respondent view).

Home market bias and the impact on global capital flow

A bias towards investing in a home market is found among liability and development sovereigns based in Western markets (91%) and in Asian markets (60%) [See Figure 2]. A key finding from the study is that some European pension funds (with liability objectives) are concerned by the perceived quality of shareholder protection on different stockmarkets and favour asset liability management and competitive advantage offered by home markets.

Scandinavian sovereigns, in particular, found disclosure and corporate governance amongst locally listed firms superior to firms listed in international markets, and even in other Western developed markets, such as the US and Europe, risks to shareholder rights are cited.

Interestingly, the trend in home market allocations in the West runs in parallel to those markets experiencing a net decrease or zero change in allocation of new assets from sovereigns around the globe. In particular, the UK and Continental Europe are the biggest net losers with global markets looking for returns elsewhere and reducing new allocations by 20% and 25%, respectively (based on net respondent view), suggesting these economies are even more reliant on capital from their own investments. In Australia and New Zealand there has been zero change. [See Figure 1]

Nick Tolchard, Co-Chair of Invesco’s Global Sovereign Group & Head of Invesco Middle East, said: “The dynamics between local and international investment influences the contestable market for asset managers and this is particularly true in key sovereign investor markets as they look to build in house asset management capability. The strong home market bias of some of the Western sovereigns has major implications for the world’s markets and suggests that future changes in shareholder protection regulation could have a significant impact on sovereign investor allocations and, as a result, on global capital flow.”

In the Middle East, the trend in home market and international market allocation is evenly split (50% each), but the story is quite different in Emerging Markets where 78% of sovereigns are allocating more to internationals markets [see figure 2]. Only 22% allocate more to home markets, indicating that these are the assets predominantly flowing around the globe. In fact over half (60%) of the capital flow from Emerging Markets is allocated to the US whose role as the world’s reserve currency and currency peg for a number of these countries makes liquid investments such as Treasuries very attractive [see figure 3].

Concerns around ‘Dutch disease’ is a key reason cited by Latin American liquidity sovereigns for low allocations to home markets (17%), where they are shifting money out of their countries to avoid currency inflation which could damage exports and potentially increase unemployment in the manufacturing sector. These sovereigns are identified as ‘liquidity’ sovereigns and this activity is in keeping with their stabilisation objectives. In the event of a crisis, highly liquid foreign assets could therefore be used to support the exchange rate and stimulate demand in the economy.

Nick Tolchard concluded: “Understanding the size and scope of geographic allocations by sovereign investors is important and can have a meaningful impact on economic growth, capital markets and the asset management community. In commissioning this independent study we have sought to focus on the trends driving investor behaviours of the major sovereign investors across the globe, and it forms part of our strategic commitment to understanding the perspective of these complex entities.”